-------------------------------

“Ask Jeff" is a weekly post made on the RyanAgency.com Blog.

Submit an insurance-related question to “Ask Jeff”.

-------------------------------

555-555-5555

mymail@mailservice.com

Unfortunately, there is no such thing as “fully insured” for any type of insurance.

That is true whether one is discussing Auto, Home, or any type of Business Insurance.

You see, though many insurance policies are very broad in the coverage they provide, exclusions and limitations exist with any program.

When discussing insurance with a potential contractor, it is always fair to ask

“What specific forms of coverage do you have in place?”

To start, a Contractor should have the following policies in their portfolio:

When requesting an estimate for work they are going to do on your behalf, you can also ask your contractor if they can provide you with a “Certificate of Insurance” that shows the types of policies and limits of the coverage they carry.

If they are “fully insured” as claimed, this should be easy to obtain. A phone call to their agent to provide the certificate directly to you as a customer is all it should take.

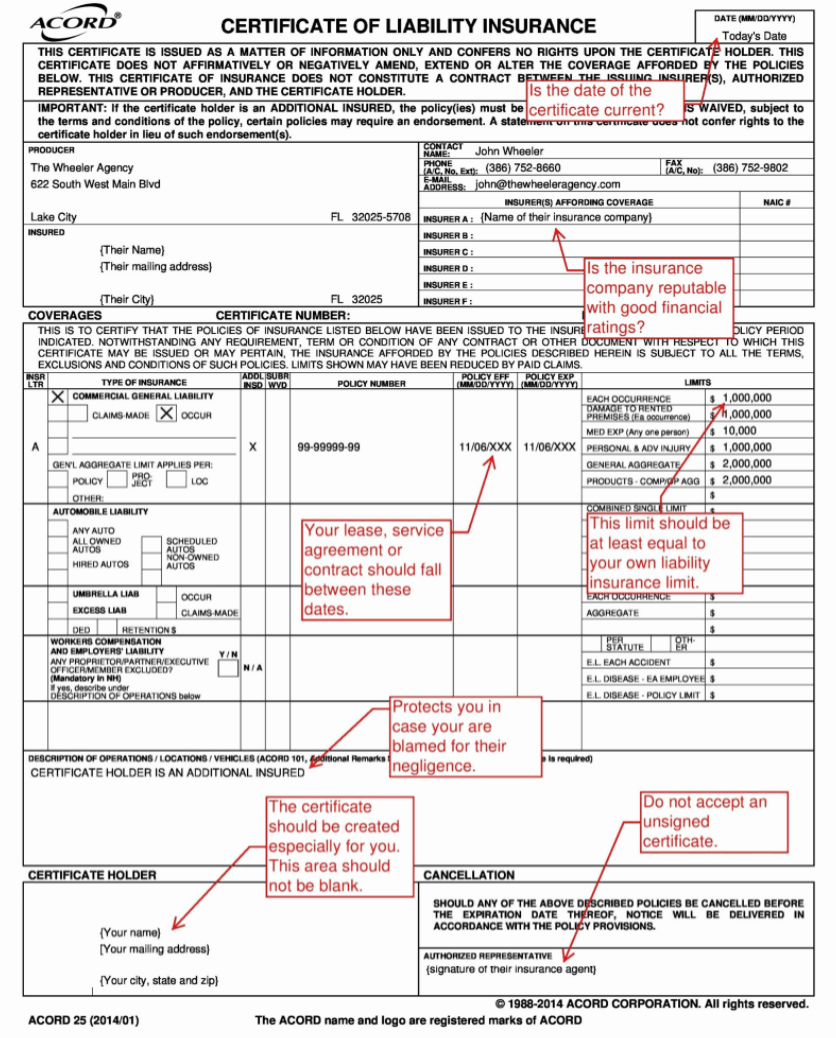

On the certificate, you might ask that the insurance agent actually state under the “Description of Operations” section, what type of contracting classifications they are insured for.

Any Certificate provided should show a current date on the top of the form and effective dates for the policies they have that fall within the date the certificate is issued. A sample Certificate of insurance can be see below:

Any contractor who purports that they are “fully insured” should be quick to provide you with a Certificate as outline above.

-------------------------------

“Ask Jeff" is a weekly post made on the RyanAgency.com Blog.

Submit an insurance-related question to “Ask Jeff”.

-------------------------------

This article may have been originally published at Quora.com.

To see Jeff's Quora.com profile click here.