-------------------------------

“Ask Jeff" is a weekly post made on the RyanAgency.com Blog.

Submit an insurance-related question to “Ask Jeff”.

-------------------------------

555-555-5555

mymail@mailservice.com

The short answer to this question is simply… Yes. Comprehensive (or Other than Collision) coverage explicitly covers Theft or Larceny, without any “ifs”. On the other hand, any auto insurance policy will contain a provision that speaks to fraud. A snippet from an ISO Auto Insurance policy, common to all 50 states in the US is below: If the insured Continue Reading

The short answer to this question is simply… Yes .

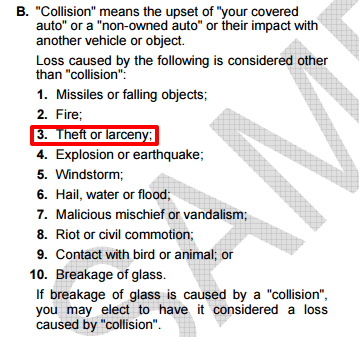

Comprehensive (or Other than Collision) coverage explicitly covers Theft or Larceny, without any “ifs”.

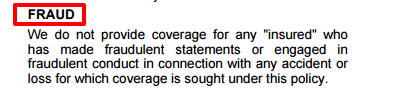

On the other hand, any auto insurance policy will contain a provision that speaks to fraud. A snippet from an ISO Auto Insurance policy, common to all 50 states in the US is below:

If the insured was complicit in a conspiracy to have the car stolen, all bets are off.

Check your policy. If an insurance company is to deny coverage for a theft because of the location of a key, an exclusion or language excepting coverage will spell it out in the Physical Damage Section (Sometimes referred to as Coverage for Damage to Your Auto) under the Insuring Agreement, Exclusions or General Provisions.

As Craig Anderson asserts, I have never read an auto policy that includes such an exclusion, nor have I ever heard of a loss such as described in this question, ever being denied.

This is no excuse for stupid behavior, but bottom line… your insurance company will cover a stolen car if you inadvertently left your key inside.

Originally posted at Quora.com: https://www.quora.com/Will-your-insurance-company-cover-a-stolen-car-if-you-left-your-key-inside

-------------------------------

“Ask Jeff" is a weekly post made on the RyanAgency.com Blog.

Submit an insurance-related question to “Ask Jeff”.

-------------------------------

This article may have been originally published at Quora.com.

To see Jeff's Quora.com profile click here.